Silver and the Limits of Paper Markets: Leverage, Physical Supply, and Industrial Demand

Silver sits at the intersection of financial leverage and real-world demand — a structure that increasingly tests the ability of paper markets to clear without stress.

Executive Snapshot

Backdrop: The global silver market remains heavily intermediated through futures and derivatives, with physical settlement representing only a small fraction of open interest.

Base Case: Elevated leverage persists as long as confidence in settlement remains intact and dilvery pressures are contained.

Risk Case: Rising industrial demand and tightening physical availability increase stress on settlement mechanisms, amplifying volatility.

Key Variables: Open interest vs. registered inventory, industrial demand growth, lease rates, and futures curve behavior.

Key Takeaways:

- Silver’s price is shaped not only by investment demand, but also by structural leverage in paper markets.

- Physical settlement is rare, but confidence in the ability to deliver is foundational to futures pricing.

- Industrial demand — particularly from technology and energy systems continues to grow, reducing supply elasticity.

- Dislocations between paper and physical markets tend to express themselves through volatility rather than linear pricing.

The Structure of the Silver Market

Silver trades primarily through futures markets, where open interest often exceeds the amount of readily available and deliverable physical silver bullion by a wide margin. This structure is not inherently problematic, as futures markets are designed for netting, not delivery. However, it relies on confidence that physical supply couldbe delivered if required.

In practice, only a small percentage of contracts ever settle in physical bullion. Most are rolled, offset, or cash-settled. As long as participants are comfortable with this structure, leverage can remain elevated without immediate consequence.

The risk emerges when demand for physical silver rises faster than the system is deisgned to accommodate.

Leverage, Settlement, and Confidence

Banks and instiutions often operate with significanty leverage in silver fdutures, using derivatives to manage exposure rather than holding the bullion outright. This is efficient under normal conditions, but it creates sensitivity to shifts in settlement expectations.

If confidence in settlement weakens, whether due to inventory constraints, rising lease rates, or delivery bottlenecks, market pariticpants may begin to reassess counterparty risk. Historically, such reassessments do not unfold gradually. They tend to surface through:

- Sudden volatility

- Rising premiums in physical markets

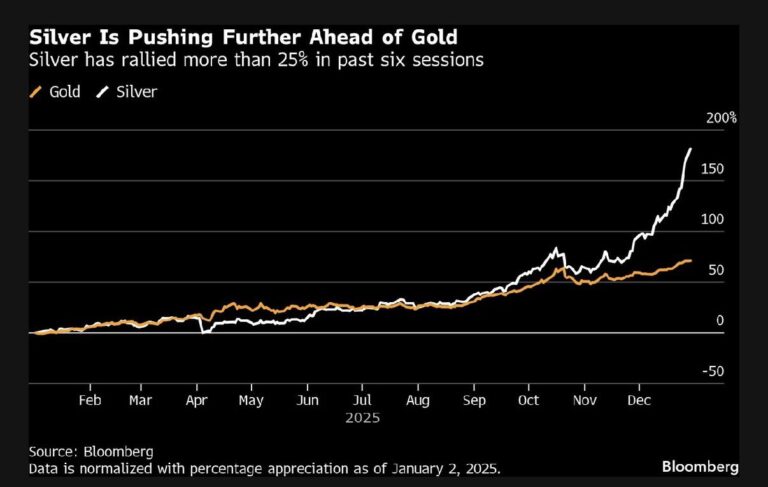

- Futures curve distortions (such as the backwardation we saw in October 2025)

Importantly, stress does not require widspread delivery failures. The perception of constraint is ofen sufficient to reprice risk.

Physical Supply and Industrial Demand

Unlike gold, silver is both a monetary metal and a critical industrial input. Demand from electronics, solar energy, and emerging tech applications has steadily increased, reducing the share of supply available for investment purposes.

The growth of AI, data centers, and electrification infrastructure has reinforced this trend. These applications rely on silver’s conductivity and durability, making substrituions difficult without performance tradeoffs.

As industrial demand absorbs a larger portion of annual production, the market’s ability to respond elastically to price signals diminishes. This increases the importance of inventories and recycling flows, which tend to adjust more slowly.

Pricing Implications

In such a structure, silver prices are not determined solely by marginal buyers and sellers, but by the balance between paper claims and physical availability.

Periods of stability can persist as long as leverage remains trusted. However, when stress emerges, repricing often occurs through sharp moves rather than incremental adjustments. This dynamic helps explain why silver has historically exhibited:

Higher volatility than gold

Episodic price dislocations

Sensitivity to shifts in confidence rather than linear demand changes

Silver’s behavior is therefore less about constant scarcity and more about periodic stress in a leveraged system.

What Would Change Our View

A reassessment of the outlook would require evidence that either leverage is being structurally reduced or physical supply is becoming meaningfully more elastic.

Key indicators to monitor include:

Inventory Dynamics: Sustained increases in registered and deliverable silver inventories.

Settlement Behavior: A continued ability to meet delivery obligations without elevated premiums or delays.

Industrial Demand: Slower growth or technological substitution reducing silver intensity in key applications.

Market Structure: A sustained reduction in open interest relative to physical availability.

Absent these developments, silver remains exposed to periodic volatility driven by the interaction between leveraged financial markets and real-world demand constraints.

AJAX Research focuses on macroeconomic analysis, fundamental research, and structured frameworks for navigating market regimes. This publication reflects research views, not investment advice.