Gold as a Regime Asset: Credibility, Real Rates, and Optionality

Gold is not a trade. It is a response to regime change and a reflection of how markets price trust, policy credibility, and the limits of financial assets.

Executive Snapshot

Backdrop: Gold’s behavior is best understood through macro regimes rather than short-term price signals.

Base Case: In policy-constrained environments, gold functions as an option on monetary credibility rather than a yield-bearing asset.

Upside Risk: Erosion in confidence around inflation control, central bank independence, or global tension increases gold’s relative appeal.

Downside Risk: Sustained positive real rates with credible policy discipline reduce gold’s opportunity cost.

Key Variables: Real rates, fiscal dominance, central bank credibility, liquidity conditions, and global tensions.

Key Takeaways:

Gold is not driven by inflation alone, but by confidence in how inflation is managed.

Real interest rates explain much of gold’s medium-term behavior, but credibility explains its regime-level moves.

Gold’s value lies in optionality, not income — it performs when policy frameworks are questioned, not when they are stable.

In times of global uncertainty, gold serves as a portfolio stabilizer rather than a return engine.

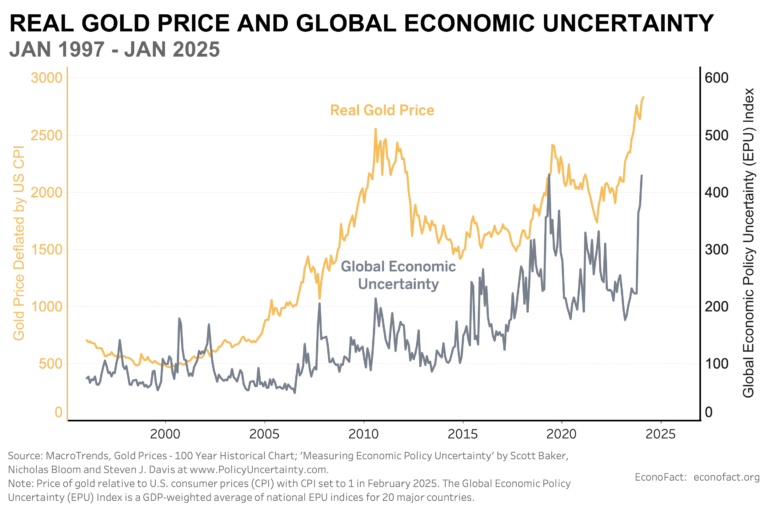

Gold Beyond Inflation

Gold is often framed as an inflation hedge, but this interpretation is incomplete. Periods of elevated inflation do not consistently coincide with strong gold performance, just as periods of low inflation do not preclude it.

What matters is not inflation itself, but the market’s confidence in policy responses to inflation.

When markets believe that monetary authorities can credibly anchor expectations, gold tends to underperform. When that credibility weakens — whether through policy error, political interference, or fiscal dominance — gold’s role becomes more relevant.

Gold responds to regime uncertainty, not data prints.

Real Rates and Opportunity Cost

The most reliable explanatory variable for gold prices over time has been real interest rates. When real yields are deeply negative, the opportunity cost of holding a non-yielding asset declines, supporting gold prices. When real yields rise and remain positive, gold often struggles.

However, real rates alone are not sufficient. There are periods when real yields appear restrictive, yet gold remains resilient. These periods tend to coincide with questions around the durability of the policy framework.

In other words, real rates describe the cost of holding gold. Credibility determines whether investors are willing to pay that cost.

Gold as an Option on Credibility

Gold functions less like a commodity and more like a long-dated option on monetary and fiscal credibility.

When confidence is high:

Capital prefers yield and growth

Financial assets dominate allocation

Gold appears redundant

When confidence weakens:

Inflation expectations become unstable

Policy reaction functions are questioned

The distribution of outcomes widens

In these environments, gold’s lack of yield becomes secondary to its role as non-financial collateral — an asset that exists outside the promise of future policy discipline.

Gold is not held for precision. It is held for asymmetry.

Geopolitical Risk and the Demand for Neutral Assets

Beyond monetary policy, gold’s role as a regime asset is reinforced during periods of heightened geopolitical tension. As global fragmentation increases and political relationships become less predictable, the value of neutral, non-sovereign assets tends to rise.

Gold occupies a unique position in this context. Unlike financial assets, it does not rely on contractual enforcement, issuer credibility, or geopolitical alignment. During periods of conflict, sanctions, or trade realignment, this neutrality becomes increasingly relevant — particularly for institutions and sovereign actors seeking to diversify away from concentrated political risk.

Recent years have seen a notable increase in central bank gold purchases, reflecting a shift toward reserve diversification amid rising geopolitical uncertainty as can be seen in the Russia-Ukraine war, tensions in the Middle East, or the current US political landscape. This demand is not driven by price expectations alone, but by a reassessment of long-term security, liquidity, and control.

Importantly, geopolitical risk does not require acute crisis to influence gold demand. Persistent tension, rather than isolated events, alters how capital is allocated over time. In such environments, gold functions as a structural hedge against uncertainty in the global order, rather than a tactical response to headlines.

Portfolio Implications

From an allocation perspective, gold should not be evaluated on expected returns alone. It should be evaluated on:

Correlation behavior across regimes

Performance during credibility shocks

Ability to preserve optionality when financial assets reprice

Gold’s utility increases when:

Real assets compete with financial claims

Fiscal considerations influence monetary outcomes

Political factors enter policy decision-making

- Global Tensions increase

It decreases when policy discipline is clear, real yields are structurally positive, and confidence remains intact.

What Would Change Our View

A reassessment of gold’s role would require evidence that policy credibility is being structurally reinforced rather than questioned.

Key signals to monitor include:

Sustained Positive Real Rates: Maintained without destabilizing growth or financial conditions.

Policy Independence: Clear separation between monetary decisions and political influence.

Anchored Expectations: Stable inflation expectations across market measures.

Fiscal Discipline: Reduced reliance on monetary accommodation to absorb fiscal pressures.

- Resolutions: Agreements between nations with heightened tensions

Absent these conditions, gold remains best understood as a regime asset — one whose relevance increases not during inflationary headlines, but during periods when the framework itself becomes uncertain.

AJAX Research focuses on macroeconomic analysis, fundamental research, and structured frameworks for navigating market regimes. This publication reflects research views, not investment advice.

For a complete analysis, data framework, and historical performance context, view the full AJAX Research – Gold Report (PDF) below.