RTX Corporation: Defense Durability in a Multi-Year Procurement Cycle

RTX is not a momentum trade. It is a position in structural defense demand, cash-flow resilience, and the stability of long-cycle procurement in an environment shaped by geopolitics rather than traditional aerospace cyclicality.

Executive Snapshot

Backdrop: We think RTX’s valuation reflects a transition from a cyclical aerospace supplier to a structurally supported defense platform with multi-year contract visibility.

Base Case: Current pricing incorporates normalized earnings and backlog support, positioning RTX as a stable cash-flow compounder rather than a valuation dislocation.

Upside Risk: Faster margin recovery at Pratt & Whitney, sustained geopolitical defense spending momentum, and aftermarket normalization could drive returns.

Downside Risk: Extended remediation timelines, defesne budget normalization or commercial aerospace softness could put pressure on margins and delay cash-flow recovery.

Key Variables: Pratt & Whitney execution, missile defense procurement cycles, commercial aftermarket recovery, and NATO spending durability.

Key Takeaways:

RTX’s earnings are mainly shaped by procurement cycles and geopolitics as much as tradition industrial fundamentals

Missile defense replenishment and NATO re-armament represent a multi-year cycle, not a one-time spike.

Current valuation of RTX suggests a fair positioning rather than a mispricing, with returns being dependent on execution.

RTX’s main function is a defensive equity compounder with a balanced upside, consistent with a neutral/hold stance.

Defense as a Structural Regime, Not a Cyclical Event

We believe this current defense environment differs fundamentally from prior cycles. Today’s spending priorities reflect structural shifts in geopolitical fragmentation, alliance re-armament, and sustained readiness requirements.

Global military spending in 2024 reached a record-breaking $2.7 trillion, driven mainly by the compounding effects of the Middle East tensions, Russia-Ukraine war, and a renewed emphasis increased NATO spending. For RTX, this backdrop is especially important as the company’s exposure centers on missile defense, sustainment programs, and lifecycle services. These are revenue streams that exhibit lower cyclicality and more predictable cash-flow conversion.

NATO Re-Armament and Diversified Demand

Since 2022, NATO members have accelerated progress toward the alliance’s 2% of GDP defense spending benchmark. The number of countries meeting this threshold has since increased materially, with several large European economies committing to a sustained multi-year budget expansion. Incremental spending is being directed toward air and missile defense, surveillance systems, and precision munitions.

This expansion reduces the historical dependence of defense demand on U.S. budget cycles. A more geographically diversified spending base would enhance revenue visibility and support backlog stability for contractors with multinational exposure, such as RTX.

Missile Replenishment as a Multi-Year Dynamic

Recent conflicts, particularly the Russia-Ukraine conflict, have depleted Western inventories of precision-guided muntions, critical defense systems, and interceptors. RTX, through the Raytheon missiles division has recently secured a 7-year agreeemtns with the U.S. DoD to scale production of Tomahawks, AMRAAMs, and SM-series interceptors. This is a strong signal for sustained demand in backlog pipelines.

Replenishment, however, differs from platform procurement. Instead of one-time purchases, it invovles sustaining orders, ongoing production runs, and lifecycle servicing. All of which, contribute to a smoother revenue realization and longer backlog duration for RTX. In turn, RTX’s exposure to missile defense systems, advanced interceptors, and classified sensing tech places the company directly within this cycle. These programs carry high margins and multi-year funding committments as well as limited competetive substitution, representing one of the most supportive elements of the current defense environment.

Commercial Aerospace as a Margin Normalizer

Beyond just defense, RTX’s commercial aerospace exposure through Collins Aerospace and Pratt & Whitney provides a nice incremental cash-flow support to the company. Collins benefits from improving flight-hours and high margin aftermarket demand, while Pratt & Whitney remans a near-term execution variable mainly due to the fact that there are inspection requirements and other remediation costs from the 2023 powder metal contamination issues. Despite these short-term headwinds, however, the largine engine base should ultimately support recurring aftermarket revenue as operational conditions normalize.

FCF Recovery as the Primary Valuation Support

RTX’s free cash flow declines in 2023 to approximately $3.8 billion due to the Pratt & Whitney remediation costs, before recovering to about $9.4 billion in 2024 and about $12.3 billion in 2025. While near-term cash conversion still slightly reflects inspection-related expenses, the normalization of remediation activity and defense damdn supports a progressive improvement in cash generation.

From a discounted cash-flow perspective, RTX’s equity value is supported by this trajectory. Sensitivty analysis across varying discount rates (WACC) and terminal growth rates indicates a reasonable valuation range rather than a mispricing.

Valuation: Fair Positioning

on a relative basis, RTX appears to be in-line with large-cap U.S. defense peers like Lockheed Martin, Northrop Grumman, and General Dynamics across forward PE and cash-flow multiples.

Improving free-cash-flow conversion and backlog visibility reduce the likelihood of meaningful downside multiple compression, which we believe positions RTX within a fair-value range across the defense sector. The company trades at a modest premium to peers, suggesting that re-rating expectations are already priced in.

Portfolio Implications

From an allocation perspective, RTX should just be evaluated just on expected returns alone, but within a broader framework:

Defensive equity exposure

Diversified revenue streams across missile defense, sustainement programs, and commercial aftermarket recovery

Cash-flow durability supported by multi-year contracts and procurement cycles

- Balanced risk-returns profile consistent with a stable compounder rather than a mispricing opportunity

What Would Change Our View

A shift from Neutral/Hold to a more constructive stance would require evidence that RTX is materially mispriced relative to its fundamental trajectory and peer group positioning.

Key signals to monitor include:

Margin Recovery Acceleration: Pratt & Whitney inspection costs declining faster than expected, supporting near-term cash-flow expansion beyond current estimates.

Defense Spending Momentum: Sustained or accelerating NATO spending commitments, particularly in missile defense and sustainment categories where RTX has concentrated exposure.

Valuation Dislocation: RTX trading at a meaningful discount to defense peers despite comparable or superior backlog visibility and cash-flow conversion.

Geopolitical Escalation: Heightened global tensions driving incremental procurement urgency and multi-year budget commitments beyond current baseline assumptions.

Absent these conditions, RTX remains best understood as a defensive equity compounder whose relevance increases during periods of geopolitical uncertainty and whose value is supported by cash-flow stability rather than aggressive growth expectations.

AJAX Research focuses on macroeconomic analysis, fundamental research, and structured frameworks for navigating market regimes. This publication reflects research views, not investment advice.

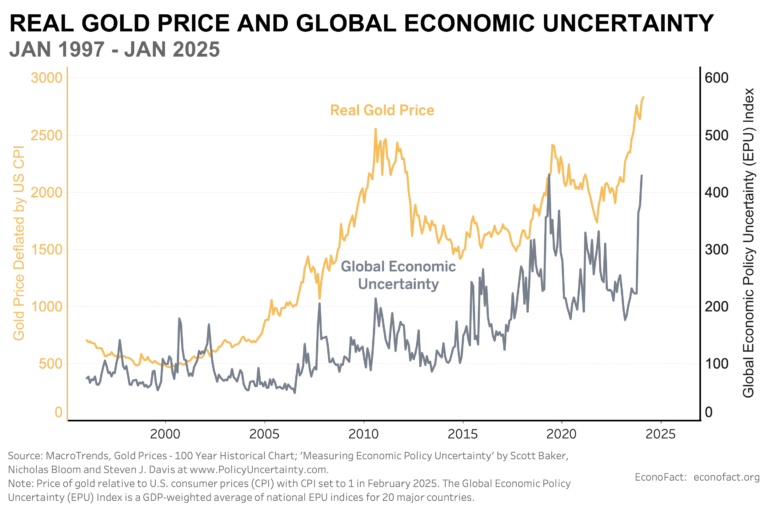

For a complete analysis, data framework, and historical performance context, view the full AJAX Research – Gold Report (PDF) below.